Understanding sequence of returns risk

Retirement organizing really should start off at the onset of your qualified occupation. Like numerous items in finance, the earlier, the better. Many residents and fellows can help save into a retirement prepare and receive matching contributions even in the course of their instruction. Around the upcoming 30-plus a long time as a clinical supplier, your financial commitment returns will enjoy a function in your preparedness for retirement, but returns are not the only vital variable. You are going to also have to handle your way of living costs, retirement financial savings, and lots of other areas of building a audio retirement approach.

Knowledge sequence of returns risk

Numerous have turn out to be acquainted with a risk around the past 15 years called the sequence of returns threat (SORR). That is, the hazard a late-vocation professional or early retiree will knowledge damaging financial investment returns. The risk will become additional well known later in your job since it gives you a lot less time to make up for losses that may well also be compounded by account distributions.

Many folks have listened to horror tales of pals and loved ones users striving to retire through the 2008 economical crisis. These horror stories exist generally because of to the sequence of returns threat.

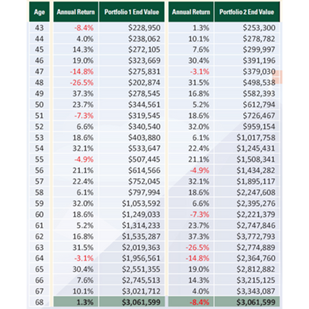

Timing matters

Choose two mid-occupation traders, in which equally traders have a portfolio sizing of $250,000 at age 43. In excess of the study course of the subsequent 25 years, just about every trader been given the very same returns but in the opposite purchase. Here are their investment decision outcomes (making use of the S&P 500 Index as their investment):

Considering that the two investors were in the accumulation period of their retirement organizing, both equally finished with the precise very same account worth inspite of the get in which their returns ended up obtained.

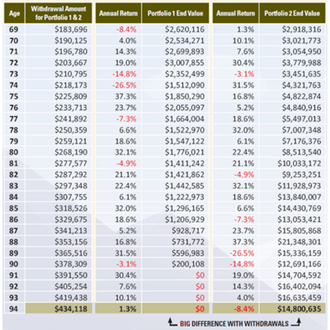

Now, get those people exact two buyers. Both of those are now at retirement and need annual distributions equivalent to 6 per cent of their portfolio in the 1st calendar year, with 3.5 per cent increases every year thereafter. Both equally buyers start off with a portfolio of $3,061,599.

As you can see, the get in which the buyers receive their investment decision returns in the course of their Distribution Section of retirement organizing will become considerably more critical through periods of withdrawals thanks to the sequence of returns risk. In the illustration higher than, the 1st trader runs out of dollars, and the second trader has a portfolio valued at $14,800,635, regardless of owning withdrawn far more than $7,500,000.

This sequence of returns threat is authentic and can have a extensive-long lasting psychological and money impression on some of the very best years of your existence.

Listed here are three action products you may possibly benefit from to mitigate the sequence of returns hazard in retirement.

1. Assessment your portfolio allocation. As you method retirement, the danger in just your portfolio or generally the publicity to shares isn’t required to be the same as at the onset of your job. Hence, as you in close proximity to your retirement date, examining your portfolio allocation will become much a lot more vital to figure out if you are aligned appropriately with your ambitions. This phenomenon occurs quickly in many employer-sponsored retirement options these types of as 401(k), 403(b), 457(b), or 401(a) plans if you are employing a Concentrate on Day Fund. For illustration, a goal date fund allocation for an individual 35 several years absent from retirement frequently has 90 p.c inventory exposure. In contrast, somebody inside of 5 yrs of retirement has roughly 55 p.c publicity to shares. In addition, not all investments or mutual funds change their exposures more than time. Therefore, you ought to review and totally fully grasp how your accounts are allotted.

2. Realize your comfort stage for volatility in the course of retirement. In 1978, Congress passed the Revenue Act of 1978, making it possible for workers to defer their income to a Portion 401(k) program. Just before this, most companies presented pension plans. Right now, and for the previous numerous yrs, this suggests the responsibility for retirement earnings preparing has shifted from an employer’s obligation to an employee’s responsibility. Thus, it is significant to establish regardless of whether you are at ease with the probable for a variable retirement cash flow approach (taking distributions from investment decision accounts as desired) or if you’d like much more security in your income setting up during retirement. Although pension designs are practically extinct, there are other options out there to assistance retirees obtain secure revenue all over retirement.

3. Hold sufficient money reserves to stay away from withdrawals in weak market many years. An additional way to decrease your sequence of returns threat would be to make the most of a bucket retirement earnings organizing tactic. To keep suitable money reserves, supplement one particular to 3 full yrs of your needed retirement money. Of course, this does build other hazards but can aid reduce the sequence of returns hazard by applying income reserves during risky sector many years and then replenishing your income reserves when your investments have recovered.

Considering retirement?

It is unachievable to predict the long term or foretell the current market surroundings when you are all set to retire. But, timing can profoundly influence your ability to maintain your earnings if you system to withdraw your accrued assets systematically.

Jordan Bilodeau is a qualified monetary planner.

Disclosure: The illustrations earlier mentioned are hypothetical and for illustrative purposes only and are not consultant of any product or service. The Common & Poor’s 500 Composite Index (S&P 500) is an unmanaged index of 500 common shares usually regarded representative of the U.S. inventory marketplace. Indexes do not think about the costs and fees linked with investing and men and women.

Securities, investment decision advisory, and money planning providers are offered through qualified Registered Reps of MML Traders Expert services, LLC. Member SIPC. Supervisory business: 4350 Congress Road, Suite 300, Charlotte, NC 28209, (704) 557-9600. Spaugh Dameron Tenny is not a subsidiary or affiliate of MML Investors Companies, LLC or its affiliated corporations. CRN202601-3761265.

:quality(70)/cloudfront-eu-central-1.images.arcpublishing.com/irishtimes/SL4ZJEXTC5DIXNN4OZFLJTU4UE.jpg)